Your Ultimate Guide to Personal Finance: Budgeting, High-Yield Savings, Credit Score & Inflation Explained

💰 Setting the Foundation: Mastering Your Budget

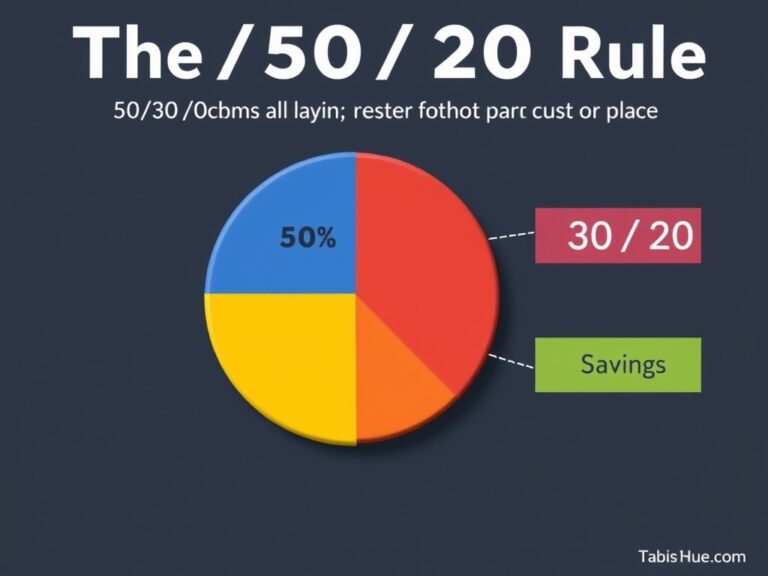

Welcome to your comprehensive guide to personal finance, where we transform complex numbers into a roadmap for your financial freedom! Budgeting is often misunderstood as a restriction, but in reality, it is simply telling your money exactly where to go instead of wondering where it went at the end of the month. One of the most effective methods for beginners and experts alike is the 50/30/20 rule, which provides a clear framework for allocation. You should aim to spend 50% of your income on ‘needs’ like housing and groceries, 30% on ‘wants’ such as dining out or hobbies, and the remaining 20% on ‘savings and debt repayment.’ To make this work, you must be honest about your spending habits and track every single transaction for at least thirty days. Using tools like spreadsheet templates or automated apps can drastically reduce the friction of maintaining this habit. Remember that a budget is a living document that should evolve as your life circumstances and goals change over time. If you find yourself overspending in one category, simply adjust another to keep your financial health in balance. Establishing this foundation is the single most important step you can take toward long-term wealth. By mastering your cash flow now, you are building the discipline required to manage much larger sums of money in the future. Let’s look at how you can optimize that 20% savings portion effectively. Consistency in tracking will eventually lead to intuitive spending habits that align with your core values. This approach ensures you are never caught off guard by unexpected expenses or lifestyle creep.

- Step 1: Calculate your total monthly take-home pay.

- Step 2: Categorize your expenses into needs, wants, and savings.

- Step 3: Set up automated transfers to your savings account.

- Step 4: Review and adjust your budget at the end of every month.

📈 Making Your Money Work: The Magic of High-Yield Savings

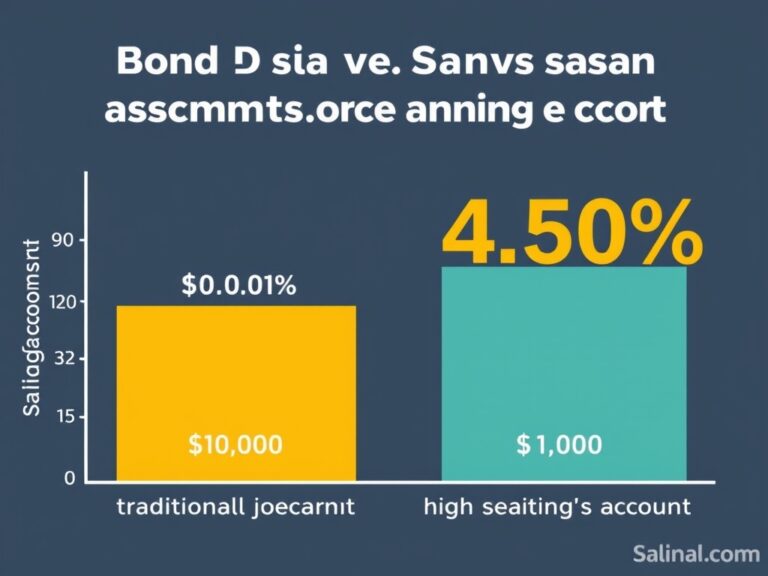

Now that you have a plan, where should you park your hard-earned cash? Most traditional banks offer a measly interest rate that barely makes a dent in your balance. This is where High-Yield Savings Accounts (HYSA) become your best friend in the financial world. Unlike standard accounts, HYSAs can offer rates that are 10 to 20 times higher than the national average. This interest is calculated as Annual Percentage Yield (APY), which reflects the real rate of return including compound interest. Compound interest is effectively ‘interest on your interest,’ helping your balance grow exponentially over time. These accounts are usually offered by online-only banks because they have lower overhead costs and can pass those savings to you. Your money remains highly liquid, meaning you can withdraw it whenever an emergency arises without any penalty. It is the perfect place for your ’emergency fund,’ which should ideally cover three to six months of living expenses. Opening one takes less than ten minutes and often requires no minimum balance to get started today. Why leave money on the table when you can let the bank pay you for keeping your money safe? Think of it as a low-risk way to beat the drag of traditional banking and build momentum. Once you see those monthly interest deposits hitting your account, you will never want to go back.

- High Returns: Earn significantly more than traditional accounts.

- Safety: Most accounts are FDIC insured up to $250,000.

- Liquidity: Access your cash quickly when needed without market risk.

💳 The Credit Score Code: Why It Matters and How to Win

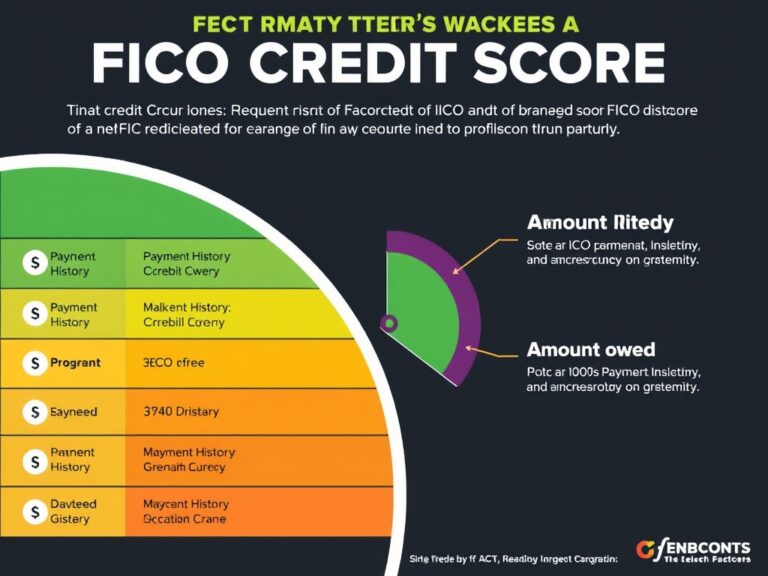

Moving along, let’s talk about your credit score, which is essentially your financial reputation or ‘Adult GPA.’ A high credit score is the key to unlocking lower interest rates on mortgages, car loans, and even insurance premiums. Your score is determined by several factors, the most important being your payment history, which accounts for 35% of the total. Another critical factor is your credit utilization ratio, which measures how much of your available credit you are actually using. Financial experts recommend keeping this ratio below 30% to maintain a healthy and robust score. The length of your credit history also matters, so it is often wise to keep older accounts open even if you don’t use them frequently. New credit inquiries can cause a temporary dip in your score, so avoid applying for multiple cards at once. You should check your credit report annually for errors that could be dragging your numbers down unfairly. Improving your score isn’t an overnight process, but consistency in on-time payments will yield massive results. Remember that your credit score is a reflection of your reliability as a borrower over the long haul. Don’t be discouraged by small fluctuations, as the trend over time is what matters most to lenders. By treating your credit with respect, you save yourself thousands of dollars in interest over your lifetime. It is a powerful tool that, when used correctly, facilitates major life purchases with ease.

- Pay every bill on time, every single time, to build a perfect history.

- Keep your credit card balances low relative to their total limits.

- Avoid closing old accounts to preserve your average credit age.

- Monitor your report for identity theft or inaccuracies once a year.

🎈 Navigating Inflation: Protecting Your Purchasing Power

Finally, we must address the ‘invisible thief’ of the financial world: Inflation. Inflation is the general increase in prices and the subsequent fall in the purchasing value of your money. This means that $100 today will likely buy fewer goods and services five or ten years from now. While a small amount of inflation is a sign of a healthy economy, high inflation can erode your savings if they aren’t growing. To protect your wealth, you need to ensure your investments earn a return that exceeds the current inflation rate. This is why investing in assets like stocks, real estate, or inflation-protected securities is so vital for long-term health. Diversifying your portfolio allows you to hedge against the rising costs of living across different sectors. While it might feel safer to keep all your money in cash, the loss of purchasing power is a guaranteed risk. Understanding the Consumer Price Index (CPI) can help you track how much prices are rising on average. Education is your best defense against economic shifts that seem outside of your direct control. By combining a solid budget, high-yield savings, and a great credit score, you create a shield against inflation’s impact. Now is the perfect time to take charge of your financial destiny and start building the life you deserve! Financial literacy is not a destination, but a continuous journey of learning and adaptation. Take the first step today by reviewing your bank statements and identifying one small change you can make.

- Invest in Equities: Historically, the stock market has outpaced inflation rates.

- Real Estate: Property values and rental income often rise in line with inflation.

- TIPS: Treasury Inflation-Protected Securities are specifically designed to adjust with the CPI.