Personal Finance Essentials: Budgeting, Boosting Credit, High-Yield Savings & Understanding Inflation

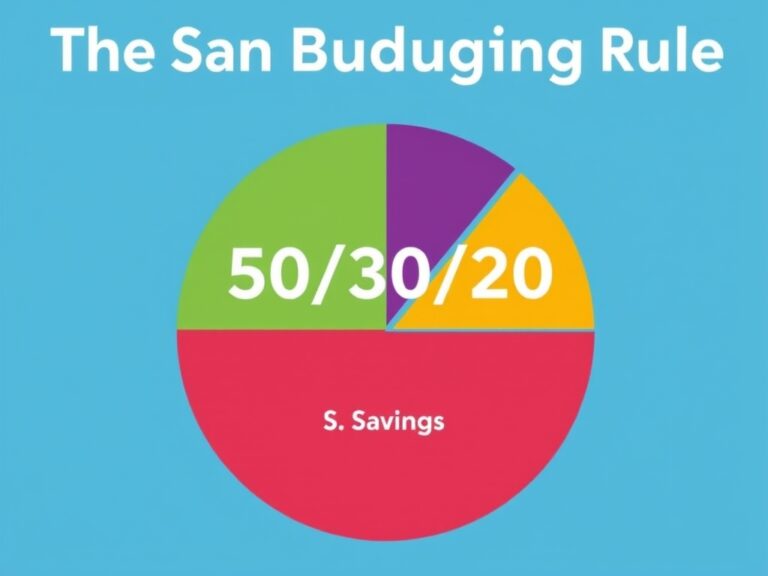

Welcome to your financial journey, where we turn “where did my money go?” into “this is where my money goes!” Budgeting is the absolute bedrock of personal finance, and it’s honestly much simpler than most people make it out to be. Think of a budget not as a cage that restricts your spending, but as a roadmap that gives you permission to spend on what truly matters to you. One of the most effective methods for beginners and experts alike is the 50/30/20 Rule, which simplifies your entire financial life into three manageable buckets.

- 50% for Needs: This covers your rent, groceries, utilities, and transportation.

- 30% for Wants: This is your ‘fun money’ for dining out, hobbies, and Netflix.

- 20% for Savings & Debt: This goes toward your emergency fund and paying down high-interest credit cards.

By automating these transfers, you ensure that your future self is taken care of before you even have a chance to spend that extra cash. Tracking your expenses is vital because it reveals patterns you might not notice, like that daily $7 latte adding up to over $200 a month. It’s about intentionality rather than deprivation, allowing you to align your spending with your personal values. When you master your cash flow, you gain a sense of peace that no impulse purchase can ever provide. Start small, stay consistent, and watch how quickly your financial landscape changes for the better.

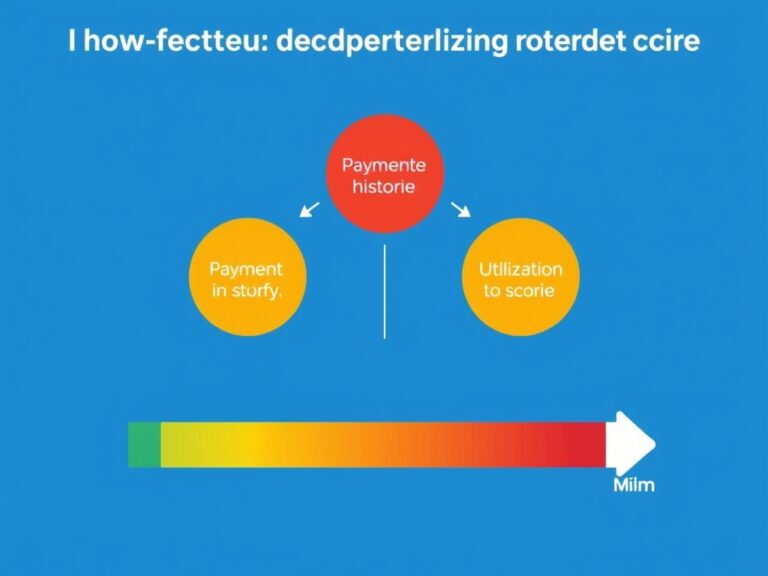

Next up, let’s talk about your Credit Score, which is essentially your financial reputation in the eyes of lenders and banks. Having a high credit score is like having a VIP pass to the financial world; it unlocks lower interest rates on mortgages, better insurance premiums, and even helps when renting an apartment. To boost your score, the single most important factor is your payment history, so never, ever miss a due date. Another critical component is your credit utilization ratio, which is the amount of credit you’re using compared to your total limits.

- Keep utilization under 30% to show lenders you aren’t overextended.

- Avoid closing old accounts, as the length of your credit history matters significantly.

- Check your credit report annually for errors that might be dragging your score down.

If you’re just starting out, a secured credit card can be a fantastic tool to build a positive history from scratch. Remember that credit is a tool, not a supplement to your income, so use it wisely and pay it off in full every month. Over time, these small habits compound, leading to a robust score that will save you tens of thousands of dollars in interest over your lifetime. It takes patience to build, but the freedom that comes with excellent credit is well worth the effort.

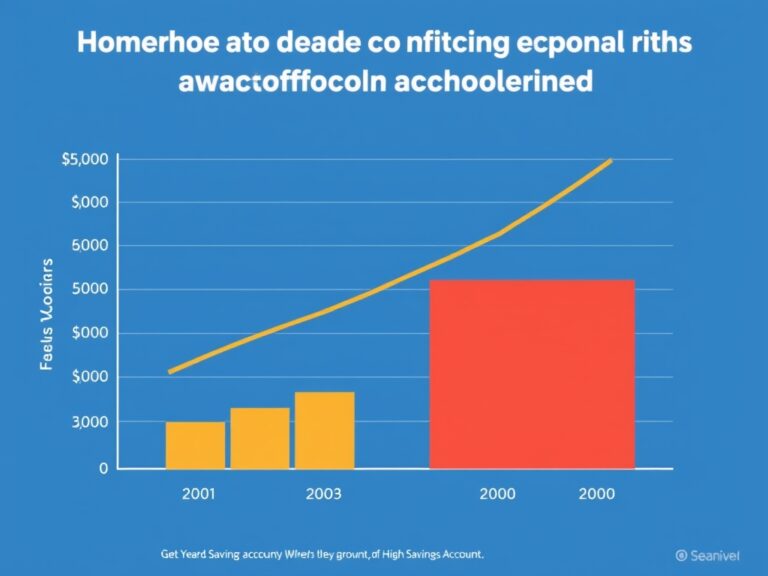

Once you have your budget and credit in check, it’s time to make your money work harder for you using a High-Yield Savings Account (HYSA). Most traditional big-name banks offer measly interest rates like 0.01%, which is basically letting your money sit idle while the bank profits. In contrast, an HYSA can offer rates that are 10 to 50 times higher, allowing your emergency fund to grow significantly through the power of compound interest. This is the perfect home for your emergency fund—that 3 to 6 months of living expenses you keep tucked away for unexpected car repairs or medical bills.

- Liquidity: You can access your money quickly if an emergency strikes.

- Safety: Most HYSAs are FDIC-insured, meaning your money is protected up to $250,000.

- Zero Effort: Once you set up an automatic deposit, your savings grow without you lifting a finger.

Think of it as a low-risk way to combat the eroding effects of time on your cash. It’s incredibly satisfying to see those monthly interest payments hit your account, knowing that your money is generating its own ‘paycheck.’ By switching to an online-only bank that offers these higher rates, you’re taking a massive step toward financial security. Don’t let your hard-earned cash rot in a standard savings account when it could be flourishing in a high-yield environment.

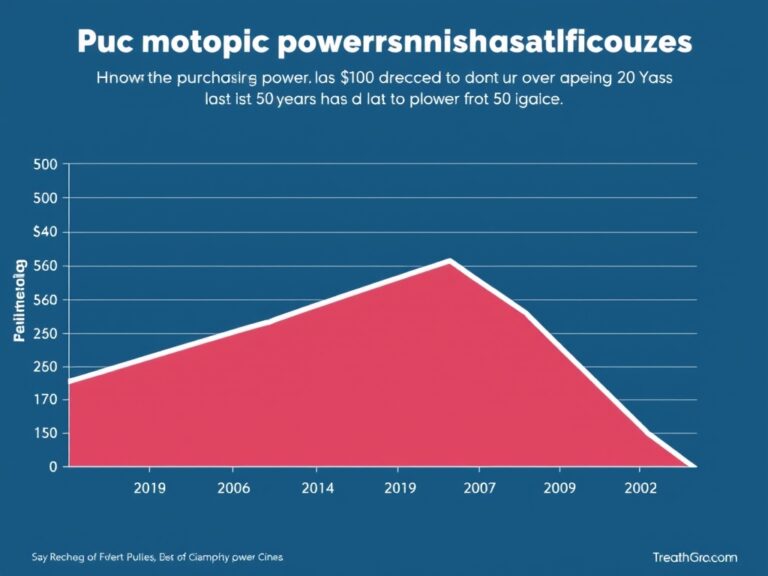

Finally, we need to address the ‘elephant in the room’ that affects every single dollar you own: Inflation. Inflation is the steady increase in the prices of goods and services over time, which means your dollar buys less today than it did yesterday. Understanding inflation is crucial because it highlights why simply ‘saving’ isn’t enough for long-term wealth—you also need to invest. If inflation is at 3% but your savings account only earns 0.01%, you are technically losing purchasing power every single year.

- Purchasing Power: The real value of your money in terms of what it can actually buy.

- Asset Classes: Investing in stocks, real estate, or commodities can help outpace inflation.

- Fixed-Rate Debt: Interestingly, inflation can benefit those with fixed-rate mortgages, as you’re paying back loans with ‘cheaper’ dollars.

To protect yourself, focus on increasing your income and investing in assets that historically grow faster than the rate of inflation. It’s all about maintaining the value of your labor over decades, not just the nominal number in your bank account. While inflation can feel scary, staying informed and diversified allows you to navigate these economic shifts with confidence. Knowledge is your best hedge against rising prices, so keep learning and stay proactive with your portfolio.