Master Your Money: Budgeting, High-Yield Savings, Credit Score Improvement & Understanding Inflation

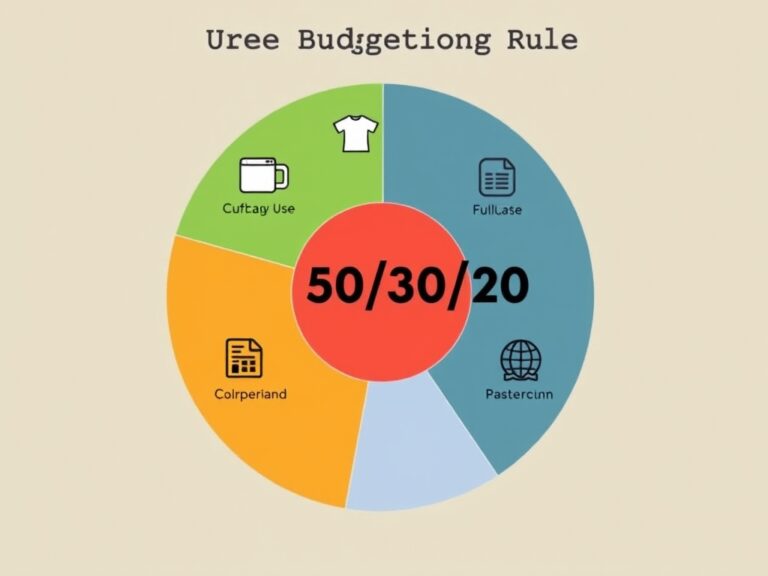

Taking control of your finances isn’t just about numbers; it’s about reclaiming your freedom and building a life where you don’t stress over every swipe of your card. Mastering your money starts with a solid foundation, and that foundation is built on the bedrock of a sustainable budget. Forget those restrictive diets for your wallet—effective budgeting is about prioritizing your goals while still allowing room for the things that make life enjoyable. A popular and effective method is the 50/30/20 rule, which simplifies your decision-making process by categorizing every dollar you earn.

- 50% for Needs: This covers rent, groceries, and essential utilities.

- 30% for Wants: This is for dining out, hobbies, and that Netflix subscription.

- 20% for Financial Goals: This goes toward debt repayment and long-term savings.

By implementing this framework, you stop wondering where your money went and start telling it where to go. It’s important to track your spending for at least 30 days to identify those ‘leaky’ expenses that drain your account. 💸 Once you see the patterns, you can adjust your lifestyle without feeling deprived or overwhelmed. Remember, a budget is a roadmap, not a cage, and it evolves as your career and life goals change. Stay consistent with your tracking apps or spreadsheets, and you’ll find that financial peace is closer than you think. This first step is crucial because you cannot optimize what you do not measure. So, let’s start today by looking at your last three bank statements and categorizing your expenses to find your baseline and start your journey.

Once you have your budget in place, it’s time to make your liquid cash work harder for you by moving it into a High-Yield Savings Account (HYSA). Traditional big-name banks often offer measly interest rates as low as 0.01%, which is essentially letting your money rot while the bank profits off your deposits. 🏦 In contrast, a high-yield account can offer rates that are 10 to 20 times higher, allowing your emergency fund to grow passively through the power of compound interest. This is where your money starts making its own money, and over time, that extra interest can add thousands to your net worth without any extra effort.

- Liquidity: Your money remains fully accessible when you need it for unexpected emergencies.

- Safety: Most HYSAs are FDIC-insured up to $250,000, ensuring your capital is protected.

- Automation: Set up recurring transfers to watch your balance climb automatically every month.

Imagine the difference between earning $1 and $400 in interest over a year—that’s the power of switching to a high-yield option. It’s an easy win that takes less than ten minutes to set up online, yet most people overlook it out of habit. 📈 Don’t let your hard-earned cash sit idle in a low-interest checking account where it loses value to the cost of living. Instead, treat your savings as a separate bucket meant for growth and security. Search for online banks with high ratings and low fees to maximize your returns. By optimizing your savings vehicle, you’re taking a proactive step toward true financial mastery and building a buffer against life’s unexpected curveballs. This is the simplest way to get a guaranteed return on your cash without taking on market risk.

Your credit score is perhaps the most powerful tool in your financial arsenal, acting as a financial passport that determines the interest rates you’ll pay on houses, cars, and personal loans. Improving your credit score isn’t about magic; it’s about understanding the specific behaviors that credit bureaus reward. The single most important factor is your payment history, so never, ever miss a due date—even if you can only pay the minimum. 💳 Another huge lever is your Credit Utilization Ratio, which is the percentage of your available credit that you’re actually using. Aim to keep this under 30%, and ideally under 10% for the best results, to show lenders you aren’t overextended.

- Check Your Reports: Use tools like Credit Karma to find and dispute errors.

- Don’t Close Old Accounts: Length of credit history matters, so keep that first card open.

- Limit New Inquiries: Applying for too many cards at once can temporarily ding your score.

Think of your credit score as a reputation score that precedes you in every major financial transaction. 📉 A high score can save you tens of thousands of dollars in interest over the life of a mortgage, essentially putting that money back into your pocket. If you’re starting from scratch, consider a secured credit card or becoming an authorized user on a family member’s established account. Be patient, as significant changes often take several months of consistent, responsible behavior to reflect in your numbers. Regularly monitoring your score helps you catch identity theft early and stay on track. By mastering these small habits, you unlock access to the best financial products on the market today.

Finally, to truly protect your wealth, you must understand the ‘silent thief’ known as inflation and how it erodes your purchasing power over time. Inflation is the general increase in prices and the fall in the purchasing value of money, meaning $100 today won’t buy as much as $100 did ten years ago. 🍞 While a little bit of inflation is normal for a healthy economy, high inflation can be devastating if your income and savings aren’t keeping pace. This is why simply ‘saving’ isn’t enough; you must eventually transition from a saver to an investor to outrun the rising cost of goods. 🛒 Assets like stocks, real estate, and even your own education are historic hedges that tend to grow faster than the inflation rate.

- Real vs. Nominal Returns: Your ‘real’ return is your interest rate minus the inflation rate.

- Purchasing Power: Focus on what your money can buy, not just the number in the bank.

- Diversification: Spread your investments to mitigate the risks associated with price volatility.

By understanding that the value of the dollar is fluid, you can make smarter decisions about when to spend and when to invest. Don’t let your wealth evaporate in a standard bank account; use your high-yield savings for short-term needs and diversified investments for the long term. 🛡️ Staying informed about economic trends helps you pivot your strategy before your budget gets squeezed. Mastering your money means looking at the big picture and ensuring that your future self is protected against the changing value of currency. When you combine budgeting, high-yield savings, and a great credit score with an awareness of inflation, you create an unbreakable financial foundation. This holistic approach ensures you aren’t just surviving the economy—you’re thriving in it for years to come.