Essential Personal Finance: Budgeting, High Yield Savings, Credit Score & Inflation Explained

💰 Let’s start with the cornerstone of all wealth: budgeting. Think of a budget not as a financial cage, but as a roadmap that gives you permission to spend without guilt. 🗺️ One of the most effective and popular strategies is the 50/30/20 rule, which allocates 50% of your income to needs, 30% to wants, and 20% to savings or debt repayment. By tracking every single dollar, you gain a sense of agency over your financial life that many people unfortunately never experience. It is absolutely crucial to distinguish between fixed expenses like rent and variable expenses like dining out or entertainment.

- Step 1: Calculate your total net monthly income.

- Step 2: List all non-negotiable bills and obligations.

- Step 3: Identify areas where you can trim unnecessary spending.

Many people find that small, recurring subscriptions add up to hundreds of dollars over the course of a year. Using modern apps or simple spreadsheets can help you visualize exactly where your hard-earned cash is going. Remember, a budget is a living document that should evolve as your life circumstances change. It is the vital first step toward building an emergency fund and eventually investing for your long-term future. Without a clear plan, even a high income can vanish into thin air without building any lasting wealth.

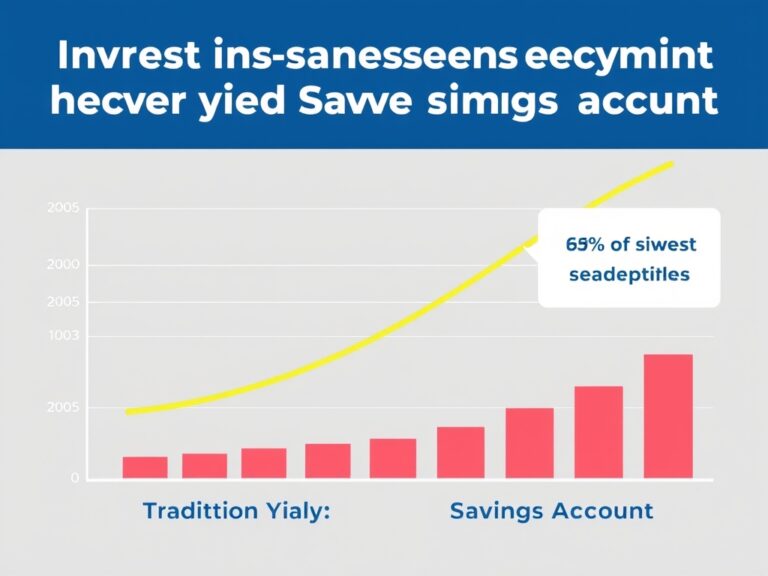

📈 Once you have your budget in place, it’s time to talk about where your emergency fund should live: a High-Yield Savings Account (HYSA). Most traditional brick-and-mortar banks offer measly interest rates that barely move the needle, but HYSAs can offer rates that are 10 to 20 times higher. This is the simplest way to make your money work for you without any market risk, as these accounts are typically FDIC insured. 🏦 Think of it as a “parking spot” for your cash that actually pays you a decent rent for staying there. The beauty of compound interest in these accounts means your savings grow exponentially over time, especially if you set up automated transfers.

- Benefit 1: Liquid access to funds whenever an emergency strikes.

- Benefit 2: Significantly higher Annual Percentage Yield (APY) than standard accounts.

- Benefit 3: Low or no monthly maintenance fees from online banks.

You should aim to keep at least three to six months of expenses here to ensure you never have to rely on high-interest debt during a crisis. It’s a foundational element of financial security that provides immense peace of mind. While it won’t make you a millionaire overnight, it protects your capital from stagnating in a low-interest environment. Don’t let your cash sit idle when it could be earning more for you every single day.

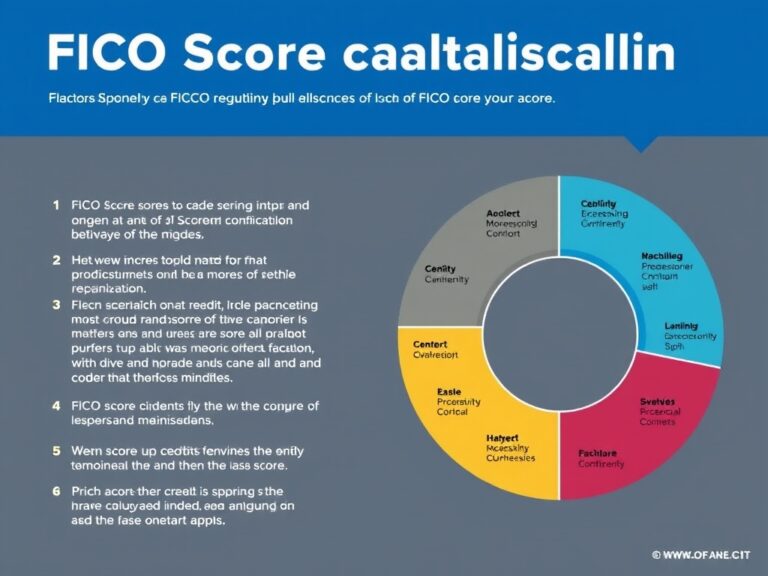

💳 Now, let’s dive into your credit score, which is essentially your financial reputation in the eyes of lenders and institutions. A high score can save you tens of thousands of dollars in interest over your lifetime by qualifying you for the best mortgage and auto loan rates. Understanding the components of your FICO score is key: payment history (35%) and credit utilization (30%) are the absolute heavy hitters. 📊 You should always strive to pay your balances in full and on time every single month to maintain a stellar record. Pro tip: Try to keep your utilization ratio below 30% to show lenders you aren’t over-leveraged or desperate for credit.

- Payment History: The most critical factor for maintaining your credit score.

- Credit Mix: Having different types of accounts like credit cards and installment loans.

- New Credit: Avoid opening too many new accounts at once to prevent score dips.

Checking your credit report annually for errors is also a vital habit to adopt for long-term health. Think of your credit score as a powerful tool; when used wisely, it opens doors to lower costs and better financial opportunities. It takes years of consistent behavior to build a great score but only a few mistakes to damage it significantly. Treat your credit score with the respect it deserves to unlock your full financial potential.

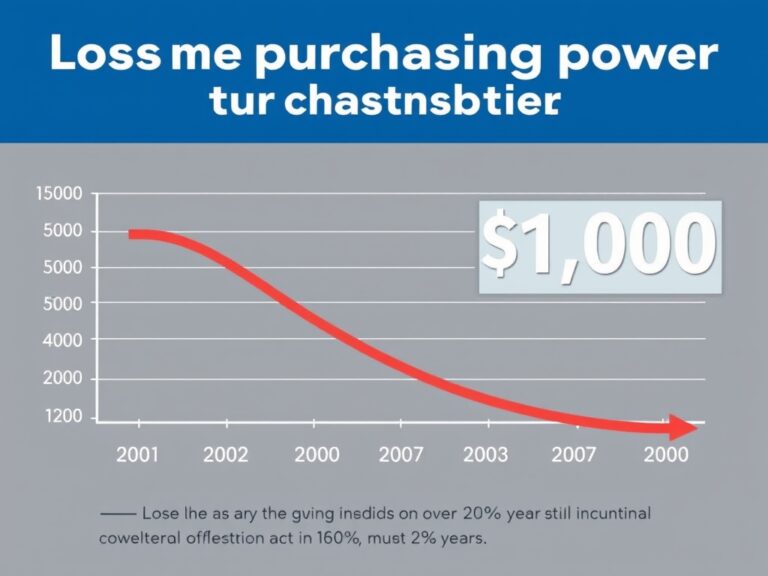

💸 We simply can’t talk about personal finance without addressing the “silent tax” known as inflation. Inflation is the gradual increase in prices and the subsequent decline in the purchasing power of your money over time. If the cost of goods rises by 3% a year but your money stays in a 0.01% interest account, you are effectively losing wealth. This is why investing becomes essential—it is the primary way to outpace inflation and grow your real wealth over the long haul. 🛡️ While high-yield savings accounts help, long-term assets like stocks, real estate, or index funds are generally needed for true growth.

- Impact: $100 today buys significantly less than $100 did ten years ago.

- Strategy: Diversify your portfolio to hedge against the rising costs of living.

- Mindset: Always focus on your “real returns” after accounting for the rate of inflation.

Understanding how the Federal Reserve manages interest rates to combat inflation can also give you a better grasp of the broader economy. Staying informed allows you to pivot your strategy when the economic climate shifts from growth to contraction. Don’t let your hard-earned savings melt away; learn to invest with intention and protect your purchasing power. Real wealth is built by staying ahead of the curve and making sure your assets grow faster than prices rise.

🚀 Bringing all these elements together—budgeting, saving, credit management, and understanding inflation—creates a robust financial ecosystem. It’s not just about how much money you make, but how much you keep and how effectively you grow it over time. Consistency is the secret sauce that turns small daily habits into life-changing wealth and security. 🌟 Start by automating your finances so that your savings and investments happen without you having to think about it every month. Financial freedom is a marathon, not a sprint, and every smart choice you make today compounds into a much better tomorrow.

- Action Item 1: Review your last three months of spending to find leaks.

- Action Item 2: Open a high-yield savings account this week to maximize interest.

- Action Item 3: Set up a recurring investment plan to build long-term assets.

Surround yourself with educational resources and don’t be afraid to adjust your plan as you learn more. You have the power to take control of your financial destiny starting right now with these fundamental steps. Stay curious, stay disciplined, and watch your financial health flourish as you reach your goals. Your future self will thank you for the discipline and foresight you are showing today.