Master Your Money: Budgeting, High-Yield Savings, Credit Scores & Inflation Explained

💰 The Foundation: Building a Budget That Actually Works

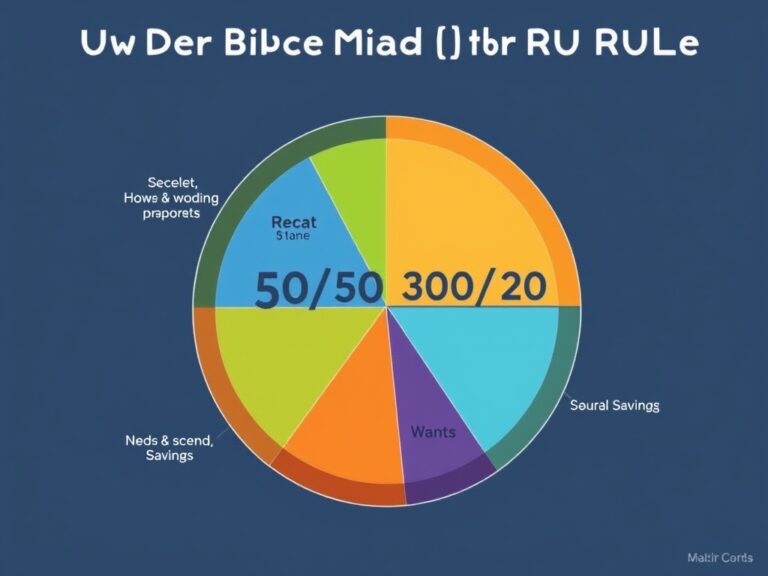

Hey there! Let’s talk about mastering your money because, let’s be honest, no one taught us this in school. The cornerstone of financial freedom is budgeting, but it doesn’t have to be restrictive or boring. Think of a budget as a roadmap for your dreams rather than a cage for your spending. One of the best methods is the 50/30/20 rule, which simplifies everything for beginners. The breakdown is quite simple to follow.

- 50% for Needs: This covers essentials like rent, groceries, and insurance.

- 30% for Wants: This allows for dining out, hobbies, and digital subscriptions.

- 20% for Savings: This is dedicated to debt repayment and your future wealth.

By categorizing your income this way, you ensure your essentials are covered while still enjoying life today. Consistency is more important than perfection when you first start your journey. Use apps or a simple spreadsheet to track every dollar for at least thirty days. You might be surprised where your money is actually going! Once you see the patterns, you can make intentional choices that align with your long-term goals. Remember, mastering your money starts with knowing exactly where it goes each month.

📈 Grow Your Money Faster with High-Yield Savings

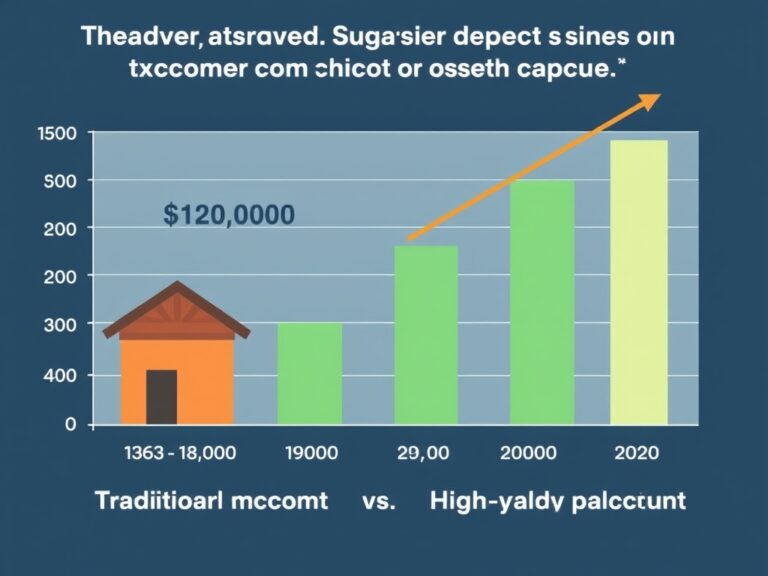

Now that you have a budget, where should you keep your hard-earned cash? Keeping all your savings in a traditional big-bank savings account is like leaving money on the table because the interest rates are often abysmal. That’s where a High-Yield Savings Account (HYSA) becomes your best friend in the financial world. These accounts often offer interest rates that are 10 to 20 times higher than standard accounts, meaning your money grows just by sitting there. It is the perfect place for your emergency fund, which should ideally cover three to six months of expenses. There are three main benefits to consider.

- Compound Interest: This is the “magic” that makes your balance snowball over time.

- Liquidity: You can still access your money quickly if an unexpected emergency strikes.

- Security: Ensure the bank is FDIC-insured so your deposits are protected by the government.

Imagine earning hundreds of dollars in interest every year instead of just a few cents. Over a decade, that difference can represent thousands of dollars in “free” money for you. Don’t let your savings lose value; move them to a high-yield home today! It’s one of the simplest steps you can take to optimize your finances with minimal effort. You worked hard for your money, so it is time your money worked hard for you.

💳 Cracking the Code: How to Master Your Credit Score

Let’s dive into something that often feels like a secret club: your credit score. This three-digit number is essentially your “adulting GPA,” and it dictates the interest rates you pay on loans and mortgages. Understanding how it’s calculated is the first step toward mastering your financial reputation. Your payment history is the biggest factor, so never, ever miss a payment if you can help it. Another huge piece of the puzzle is credit utilization, which is how much of your available credit you are actually using. To keep your score healthy, follow these simple rules.

- Keep your credit utilization under 30% to see your score climb significantly.

- Avoid opening too many new accounts at once, as this can lower your average account age.

- Check your credit report for errors regularly to ensure your information is accurate.

A high credit score can save you tens of thousands of dollars over your lifetime in lower interest costs. It opens doors to better credit card rewards and premium financial products. Treat your credit like a reputation; it takes time to build and seconds to damage. If your score is low, don’t panic, as consistent on-time payments will heal it over time. Mastering credit is about playing the long game and staying disciplined every single month.

🎈 Inflation 101: Why Your Dollar Buys Less and How to Fight Back

Have you noticed that your grocery bill is creeping up even though you’re buying the same items? That is inflation in action, and it is the silent thief of your purchasing power over time. Inflation is the general increase in prices, which means each dollar you own buys a smaller percentage of a good or service. While a little inflation is considered normal for a healthy economy, high inflation can erode your savings if you aren’t careful. This is why just “saving” isn’t enough; you eventually need to invest to outpace the rising costs of living. Understanding these three concepts will help you fight back.

- Purchasing Power: The actual value of your money in terms of what it can buy today.

- Fixed-Rate Debt: Inflation can actually benefit you here, as you pay back loans with “cheaper” dollars.

- Asset Growth: Real estate and stocks often rise in value alongside or faster than inflation.

By understanding that the value of cash decreases over time, you can make better decisions about where to put your wealth. Don’t let your future self get priced out of the lifestyle you want to live. Diversifying your assets is the best defense against the fluctuating value of the dollar. Stay informed, stay invested, and stay ahead of the economic curve. Knowledge is the only tool that doesn’t lose value over time.

🚀 Putting It All Together for Long-Term Wealth

Finally, let’s look at how all these pieces fit together to create a rock-solid financial future. Mastery isn’t about one single “win,” but about the synergy between your budget, your high-yield savings, your credit health, and your protection against inflation. When you have a budget, you have the surplus to fund your HYSA. With a strong credit score, you can leverage low-interest debt to buy assets that grow faster than inflation. It’s a beautiful cycle that builds real, lasting wealth over several decades. Follow this simple checklist for long-term success.

- Set clear, measurable financial goals for every year of your life.

- Automate your savings so you don’t even have to think about it every payday.

- Continuously educate yourself on new financial trends and modern investment tools.

You don’t need to be a Wall Street expert to achieve financial independence; you just need a plan and the discipline to stick to it. Every small decision you make today—like skipping a trivial purchase or checking your credit report—compounds into a massive advantage later. Your future self will thank you for taking the time to understand these concepts now. Financial freedom isn’t a destination; it’s a way of living with intention and security. Start today, and watch your financial world transform for the better!