The Ultimate Personal Finance Guide: Budgeting, High-Yield Savings, Credit Score & Inflation Explained

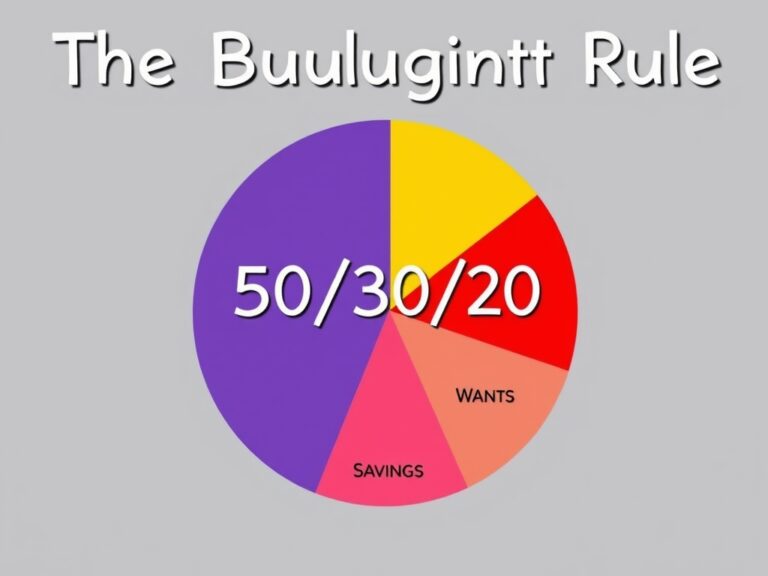

Hey there, let’s talk about the bedrock of your financial future: budgeting. Many people view a budget as a financial straightjacket, but I want you to see it as a roadmap to freedom because it tells your money exactly where to go instead of you wondering where it went. A great starting point is the 50/30/20 rule, which allocates 50% of your income to needs, 30% to wants, and 20% to savings or debt repayment. To make this work, you must track every single cent using apps or a simple spreadsheet to identify ‘spending leaks’ that drain your bank account. Audit your monthly subscriptions for unused services and set realistic limits for dining out to keep your costs under control. By giving every dollar a job, you stop emotional spending and start intentional living that aligns with your values.

- Identify fixed costs like rent and utilities.

- Categorize your discretionary spending.

- Prioritize your debt repayment strategy.

Remember, consistency beats intensity every time when it comes to managing your monthly cash flow. This transparency allows you to make informed decisions about your future large purchases without the stress. It’s about balance, not deprivation, so don’t forget to leave room for the things that actually bring you joy. Once your budget is automated, you’ll feel a massive weight lift off your shoulders and gain immense clarity. You become the master of your finances rather than a victim of your economic circumstances. Small changes today lead to massive wealth accumulation over several decades of smart planning. Let’s build a foundation that supports your wildest dreams and professional aspirations!

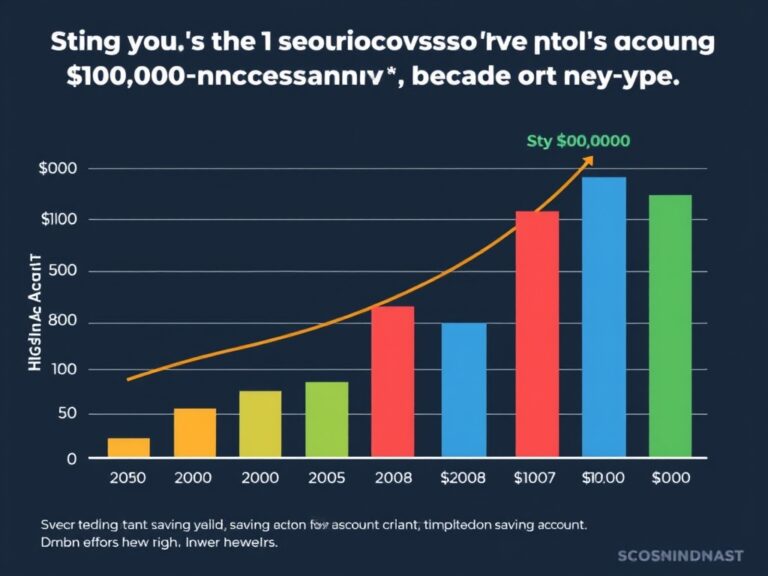

Now that your budget is set, let’s look at where that 20% savings should live, specifically in a High-Yield Savings Account (HYSA). Traditional ‘big bank’ savings accounts often offer measly interest rates like 0.01%, which is essentially letting your money rot in a vault. In contrast, an HYSA can offer 4% to 5% APY, allowing your money to grow through the magic of compound interest while remaining liquid. This is the perfect home for your Emergency Fund, which should ideally cover 3 to 6 months of living expenses. Why leave money on the table when online-only banks can pass their lower overhead costs on to you in the form of higher rates?

- Ensure the bank is FDIC insured up to $250,000 for safety.

- Check for ‘no monthly maintenance fees’ to keep all your gains.

- Look for accounts with easy mobile transfer capabilities for convenience.

Think of it as a low-risk way to fight back against the eroding power of the general economy. Even a few hundred dollars in interest per year can make a significant difference in your long-term goals. Don’t let your hard-earned cash sit idle; make it work for you while you are sleeping. Most people find that once they see those monthly interest payments hit, they become addicted to saving even more. It’s one of the simplest financial upgrades you can make today with almost zero effort or risk. You are essentially getting paid to keep your money safe and accessible for when you need it most. Researching the best rates online takes less than fifteen minutes of your time but pays off for years. Set up an automatic transfer from your checking to your HYSA every payday to ensure consistent growth.

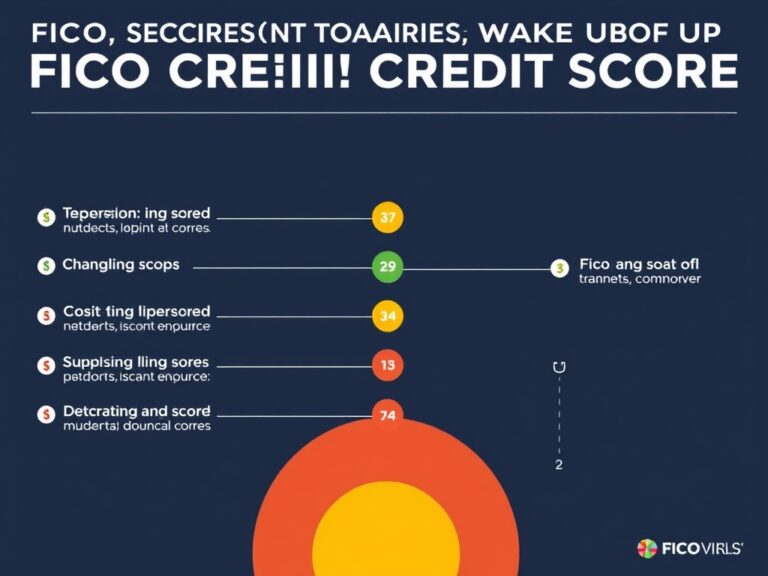

Moving on to a crucial piece of the puzzle: your Credit Score, which acts as your financial reputation in the eyes of lenders. A high score isn’t just a number; it’s a powerful tool that unlocks lower interest rates on mortgages, car loans, and insurance. To master this, you need to understand the five key components: Payment History (35%), Amounts Owed (30%), Length of History, New Credit, and Credit Mix. The most important rule is to never miss a payment, as a single delinquency can tank your score by dozens of points.

- Keep your credit utilization below 30% of your total available limit.

- Avoid opening too many new accounts in a short period of time.

- Monitor your credit report regularly for errors or potential identity theft.

Building credit is a marathon, not a sprint, requiring patience and discipline over several years of responsible use. Think of your credit score as an investment in your future ability to borrow money cheaply when needed. A 760+ score could save you tens of thousands of dollars in interest over the life of a home mortgage. It’s about proving that you are a reliable borrower who respects the capital lent to you by institutions. If you have a low score, start by paying down credit card balances immediately to see a quick bump. Using credit cards like debit cards—paying the full balance monthly—is the ultimate secret to a perfect score. Don’t close your oldest accounts, as the length of history significantly helps your total score. Check your score for free using reputable apps to stay informed of any changes to your profile.

Finally, we have to address the ‘silent thief’ of wealth: Inflation, which slowly eats your savings. Inflation is the gradual increase in prices and the subsequent fall in the purchasing power of your money over time. If the inflation rate is 3% and your money earns 0%, you are effectively losing 3% of your wealth every year. This is why just ‘saving’ isn’t enough; you must eventually transition into investing to stay ahead of the curve.

- Inflation affects everything from groceries and gasoline to healthcare and housing.

- Assets like stocks, real estate, and commodities historically outpace inflation.

- Diversification helps protect your portfolio from sector-specific price spikes or drops.

Understanding the difference between Nominal Returns and Real Returns is vital for your long-term financial success. While you can’t control federal interest rates or global supply chains, you can control your investment exposure. By investing in productive assets, you ensure that your future self can afford the same lifestyle you enjoy today. It’s the difference between merely surviving and actually thriving in an ever-changing economic landscape. Don’t be afraid of market volatility; be afraid of the guaranteed loss of value that comes from holding cash. Inflation makes the cost of living more expensive, so your income and assets must grow even faster. Investing in your own skills and education is also a great personal hedge against inflationary pressures. Real estate often performs well because rent prices tend to rise alongside general inflation over many years. Knowledge is your best defense against the rising costs of the modern world and economic shifts.

To bring everything together, remember that personal finance is personal—there is no one-size-fits-all strategy for everyone. You start with a budget to control the flow, use a High-Yield Savings Account to protect your cash, and build a Credit Score to leverage cheap debt. Finally, invest your surplus to beat inflation and build long-term generational wealth for your family. The goal isn’t just to accumulate digits, but to create financial peace of mind and future security.

- Set up automated transfers to your savings and investment accounts every month.

- Review your financial goals every quarter to stay on track with your progress.

- Educate yourself continuously by reading books and listening to reputable podcasts.

You have the power to change your financial trajectory starting today, regardless of where you began. Financial literacy is a superpower that pays dividends for the rest of your life in many ways. Success is built on the daily habits you establish now, not just the big wins down the road. Stay disciplined, stay curious, and keep your eyes on the long-term horizon for the best results. Your future self will thank you for the hard work and discipline you’re putting in right now. Don’t let fear or confusion stop you from taking the first step forward toward your goals. Every dollar saved and invested today is a seed planted for a much brighter financial tomorrow. Congratulations on taking the first step toward total financial mastery and independence!