Boost Your Finances: Budgeting, High-Yield Savings, Credit Score Improvement & Inflation Insights

1. The Foundation: Mastering Your Monthly Budget 🏰

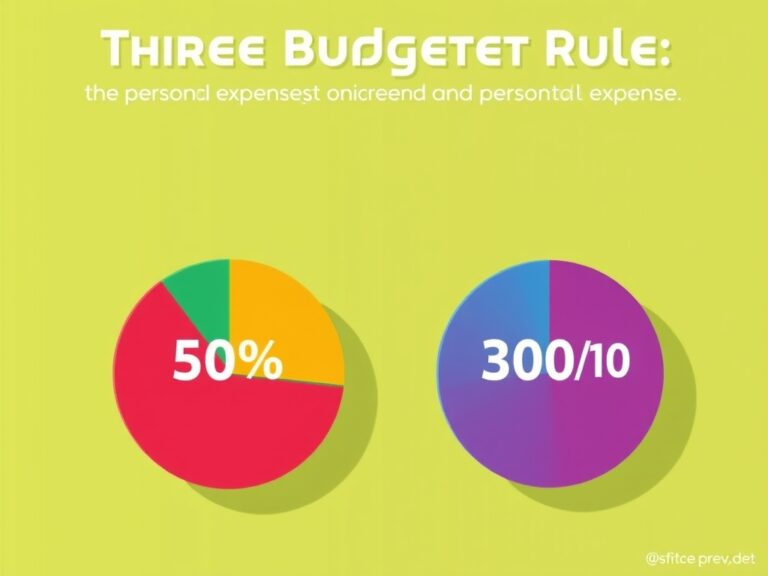

Hey there, let’s talk about building your financial fortress from the ground up! Budgeting isn’t about restriction; it’s about giving every dollar a job so you can live your best life without constant stress. Have you ever wondered where your paycheck goes by the middle of the month? By implementing a solid budgeting strategy, you reclaim control over your hard-earned money and prioritize what truly matters to you. One of the most effective methods is the 50/30/20 rule, which helps you manage your cash flow effectively.

- 50% for Needs: Essential costs like rent, groceries, and utilities.

- 30% for Wants: Discretionary spending like dining out or hobbies.

- 20% for Savings: Debt repayment and building your future wealth.

This simple framework takes the guesswork out of your monthly habits and provides a clear roadmap. To “Boost Your Finances,” start by tracking every single expense for thirty days using an app or a simple spreadsheet. 📱 You might be surprised to see how much those small, daily subscriptions add up over time. Understanding your cash flow is the first step toward achieving your long-term goals and building wealth. Once you see the patterns, you can make informed adjustments to your lifestyle without feeling deprived. Remember, a budget is a living document that should evolve with your needs as they change. 📈 Consistency is the secret sauce that turns a simple plan into a powerful financial reality. By staying disciplined, you are essentially buying your future freedom one month at a time. Start today and watch your stress levels drop as your savings rise.

2. Accelerate Growth with High-Yield Savings 💰

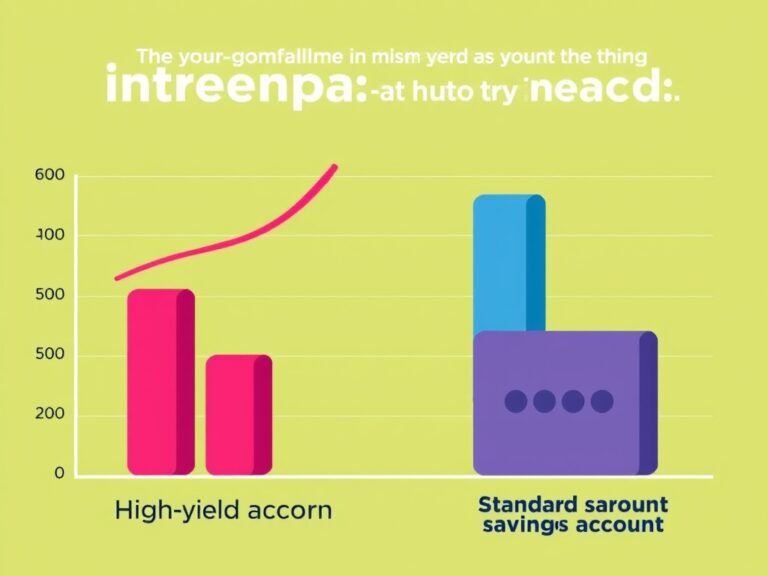

Now that you’ve mastered your budget, let’s talk about making your money work harder in a High-Yield Savings Account (HYSA). Most traditional banks offer measly interest rates that barely move the needle, effectively letting your money lose value over time. In contrast, an HYSA can offer interest rates that are significantly higher—sometimes 10 to 20 times the national average! 🚀 This is an absolute game-changer for your emergency fund or short-term goals like a down payment on a house. By parking your cash here, you benefit from the magic of compound interest, where you earn interest on your interest. Imagine watching your balance grow every month just for keeping your money in the right place. It’s a low-risk way to ensure your liquid assets are actually generating a meaningful return. 🏦 When looking for the right account, pay attention to factors such as:

- Monthly maintenance fees that eat into your earnings.

- Minimum balance requirements that might lock up your liquidity.

- The speed of transfers between your checking and savings accounts.

These accounts are specifically designed to help you outpace the slow creep of inflation while keeping your money safe. Think of it as a safety net that grows autonomously while you sleep or focus on your career. Most digital-only banks can afford these higher rates because they have less overhead than physical branches. Don’t leave your money sitting idle in a standard checking account when it could be thriving elsewhere. Taking this simple step today can lead to hundreds of dollars in “free” money over the next year. You’ve worked hard for your money, so it’s time it returned the favor.

3. Elevate Your Credit Score for Future Opportunities 💳

Let’s shift gears to credit score improvement, which is essentially your financial reputation in the eyes of the modern lending world. A higher score doesn’t just look good on paper; it saves you thousands of dollars in interest on mortgages, car loans, and credit cards. If your score is currently lower than you’d like, don’t panic—it’s a dynamic number that you can influence with the right daily habits. The most significant factor in your score is your payment history, so never miss a due date, even if you only pay the minimum. 🗓️ Another critical component is your credit utilization ratio, which is the amount of credit you’re using compared to your total limit. Aim to keep this ratio below 30% to signal to lenders that you are a responsible and low-risk borrower. 📉 You should also avoid opening too many new accounts in a short period, as this can lead to multiple “hard inquiries” that temporary dip your score. Over time, the age of your credit history also plays a vital role, so think twice before closing your oldest accounts. 🗝️ Regularly checking your credit report for errors is another pro tip that can provide an instant boost if you find inaccuracies. 🔍 Improving your score is a marathon, not a sprint, requiring both patience and financial discipline. By focusing on these core areas, you’ll open doors to better financial opportunities and much lower borrowing costs. 🚪✨ Remember that a high credit score is a tool that gives you leverage when you need it most. Consistent effort today pays off in the form of lower interest rates for years to come. You deserve the peace of mind that comes with a healthy credit profile.

4. Defending Your Wealth Against Inflation 🎈

We cannot discuss modern finances today without addressing Inflation Insights and how they impact your long-term purchasing power. Inflation is the gradual increase in prices and the fall in the purchasing value of money, and it can eat away at your savings. While you can’t control the global economy, you can certainly control your personal response to rising costs. 🛒 One strategy is to invest in assets that historically outpace inflation, such as diversified index funds or high-quality real estate. 🏠 Additionally, being a savvy consumer means looking for value and adjusting your spending habits when prices spike on specific goods. Understanding the Consumer Price Index (CPI) can help you track which sectors are being hit hardest by price hikes. 📊 It’s also a great time to negotiate your recurring bills or switch to more cost-effective service providers. When inflation is high, the “real” value of any fixed-rate debt you have actually decreases, which is a small silver lining. ☁️ However, the goal is always to ensure your income or investment returns grow faster than the cost of living. Stay informed by reading financial news and understanding how interest rate hikes by central banks aim to curb inflation. 📰 Knowledge is your best defense against economic volatility and market fluctuations. Being proactive allows you to maintain your lifestyle even when the economy feels uncertain or volatile. 🛡️ This holistic approach ensures that your wealth is protected and continues to grow regardless of the economic climate. Your financial future depends on your ability to adapt to these changes.