Personal Finance Essentials: Budgeting, High-Yield Savings, Credit Score Improvement & Inflation Explained

Mastering Your Money: The Budgeting Blueprint

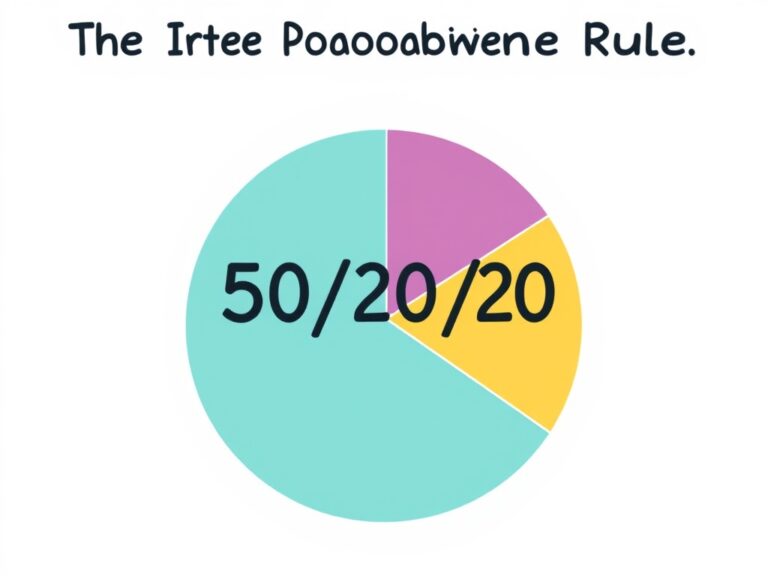

Welcome to your journey toward financial freedom, where we turn “money stress” into “money mastery” through the lens of Personal Finance Essentials. Understanding these basics isn’t about deprivation; it’s about making your hard-earned money work as hard as you do every single day. The first foundational pillar is Budgeting, which provides a clear roadmap for every dollar you earn before the month even begins. Many experts recommend the 50/30/20 Rule: 50% for needs, 30% for wants, and 20% for savings or debt repayment. This simple system ensures you cover your essentials while still enjoying life and building a secure future. To get started today, you should follow these simple steps:

- Track your total expenses for at least 30 days to see where money goes.

- Identify “leaks” like unused subscriptions or excessive dining out.

- Automate your transfers to savings accounts to remove temptation.

By visualizing your cash flow, you regain total control over your lifestyle and long-term goals. Remember, a budget is not a cage; it is actually a blueprint for achieving your wildest dreams. 📊 Small adjustments today lead to massive, life-changing results tomorrow if you remain consistent. Consistency is the secret sauce that transforms a simple plan into a wealth-building engine. Don’t worry if you slip up occasionally; the goal is always progress over perfection. Setting up this foundation allows you to breathe much easier when unexpected costs inevitably arise.

Put Your Cash to Work: High-Yield Savings Accounts

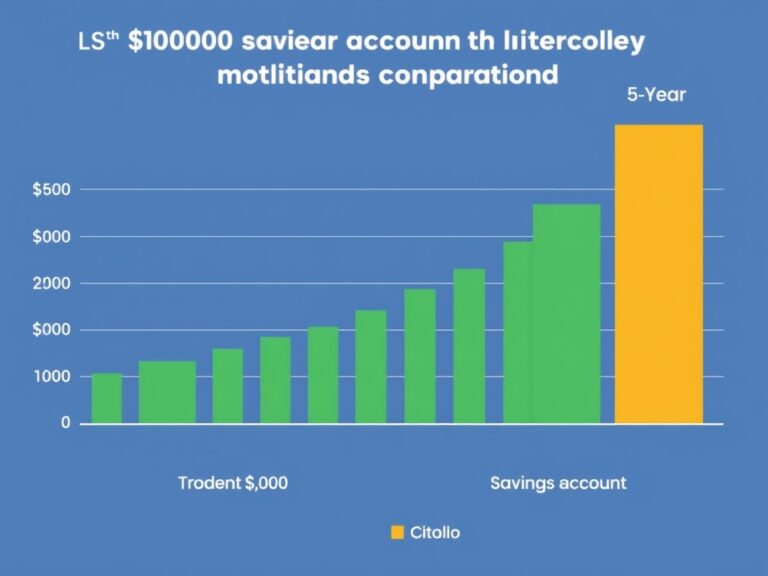

Once your budget is set, you need a safe place for your cash to grow, which brings us to the importance of High-Yield Savings Accounts (HYSAs). Most traditional big-name banks offer measly interest rates that barely move the needle, but an HYSA can offer 10x to 20x the national average interest rate. 🚀 This is the perfect home for your Emergency Fund, which should ideally cover three to six months of your living expenses. Because these accounts are typically FDIC-insured, your principal is safe while you earn a much higher Annual Percentage Yield (APY). Think of it as a low-risk way to combat the eroding effects of time on your liquid cash reserves. Here is why HYSAs are absolutely essential for your immediate financial health:

- Compound Interest: Your interest earns interest, which significantly accelerates your growth.

- High Liquidity: You can access your money quickly whenever a true emergency strikes.

- Zero Market Risk: Unlike the stock market, your balance won’t drop due to daily volatility.

Opening one is usually a quick online process that takes less than ten minutes to complete. It is honestly one of the easiest “wins” in personal finance because it requires zero effort once established. Every dollar sitting in a standard checking account is essentially losing value to time, so moving it is a massive upgrade. It’s all about being intentional with where your “lazy money” resides so it can grow for you. This simple switch ensures your safety net is actually growing while it sits there waiting for a rainy day.

Cracking the Code: Credit Score Improvement Strategies

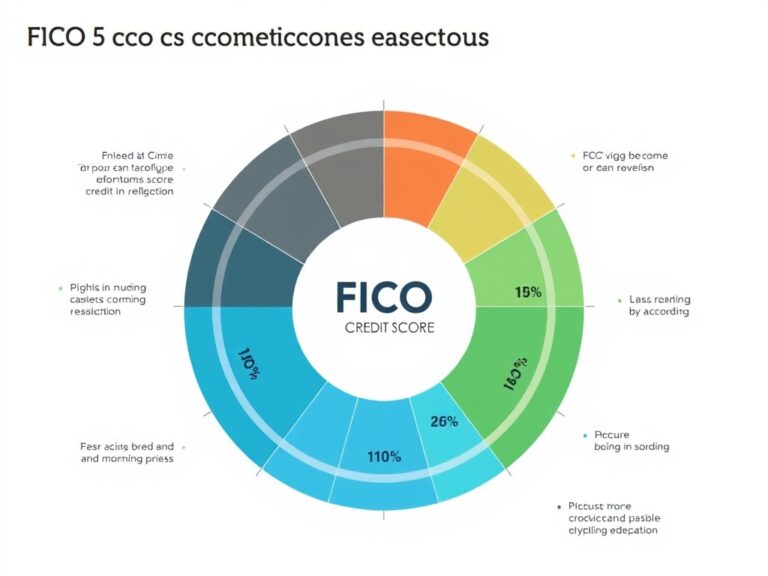

Moving on to your financial reputation, let’s talk about Credit Score Improvement and why it matters much more than you might think. Your credit score is essentially a grade of your financial reliability, influencing everything from mortgage rates to your monthly insurance premiums. 💳 A higher score can save you hundreds of thousands of dollars in interest over your entire lifetime. To boost your score effectively, you must understand the two heavy hitters: Payment History (35%) and Credit Utilization (30%). This means paying every single bill on time, every time, and keeping your credit card balances well below 30% of your total limit. 📉 If you’re looking for quick wins to jumpstart your score, consider implementing these strategies:

- Request a credit limit increase from your bank to automatically lower your utilization ratio.

- Become an authorized user on a family member’s long-standing, well-managed account.

- Dispute any inaccuracies or old errors on your credit report immediately.

Improving your credit is definitely a marathon, not a quick sprint, but the rewards are truly profound. It opens doors to the best financial products and gives you massive leverage when negotiating with lenders. 🏗️ Think of your credit score as a financial tool that, when sharpened, makes building wealth much smoother. Even a 50-point jump can move you from a “fair” to a “good” tier, drastically changing your borrowing power. Staying diligent with your balances and payments is the most effective way to secure your financial future today.

Beating the Silent Thief: Inflation Explained

Finally, we must address the “silent thief” of the global economy: Inflation Explained. Inflation is defined as the general increase in prices and the subsequent fall in the purchasing value of your money over time. 🎈 While a little inflation is considered healthy for a growing economy, high rates can quickly eat away at your hard-earned savings. This is exactly why simply saving money isn’t enough; you must also invest to stay ahead of the rising cost of living. When the cost of milk, gas, and rent goes up, your money’s “buying power” goes down, meaning you can buy less today than yesterday. To protect yourself from inflation’s grasp, consider these expert-level investment insights:

- Invest in Real Assets: Stocks and real estate have historically outperformed inflation over decades.

- Diversify Your Portfolio: Don’t put all your eggs in one basket to mitigate economic risks.

- Increase Your Earning Power: Developing new skills is the ultimate inflation-proof asset.

Understanding this concept helps you realize that cash is essentially a melting ice cube in a high-inflation environment. 🧊 By combining a solid budget, a high-yield savings cushion, and a strong credit profile, you’re better equipped to handle shifts. Personal finance isn’t just about math; it’s about behavior, strategy, and staying informed about the world around you. Take these essentials, apply them consistently, and you’ll find yourself on a fast track to true financial independence. You have the tools now—it’s time to put them into action and watch your personal wealth flourish for years to come.