The Ultimate Personal Finance Guide: Budgeting, High-Yield Savings, Credit Scores & Inflation Explained

Welcome to your ultimate personal finance guide, where we turn complex money concepts into actionable steps for your financial freedom! 💰 Budgeting isn’t about restriction; it’s about giving every dollar a job so you can live life on your terms without stress. I highly recommend starting with the 50/30/20 rule, a simple yet effective framework for managing your income efficiently. Here is how it breaks down for most successful households:

- 50% for Needs: Essential expenses like housing, groceries, and utilities.

- 30% for Wants: Discretionary spending like dining out, hobbies, and entertainment.

- 20% for Financial Goals: Aggressive debt repayment and long-term savings.

By tracking your spending through user-friendly apps or custom spreadsheets, you gain total clarity over where your hard-earned cash is going each month. Remember, the goal is progress over perfection, so do not beat yourself up if one month is a bit off-track. As you get comfortable with these numbers, you will notice that conscious spending allows you to afford what you truly value. Setting up an automated system for these categories can significantly reduce decision fatigue and ensure you stay consistent. This foundational step is the bedrock of all successful financial strategies for long-term wealth building. Without a clear budget, even a high income can vanish into thin air, leaving you wondering where it all went. Let’s commit to mastering this habit today to secure your tomorrow!

Once your budget is set, it is time to talk about where your cash sits, specifically your emergency fund and short-term savings goals. 🏦 Most traditional brick-and-mortar banks offer measly interest rates that barely move the needle on your balance over time. This is where High-Yield Savings Accounts (HYSA) become your best friend, often offering 10 to 20 times the national average interest rate. Imagine your money working for you while you sleep, compounding day by day without any extra effort or risk on your part. These accounts are usually FDIC-insured, meaning your principal is just as safe as it would be in a big-name local bank. When choosing the right account for your needs, look for these specific features:

- No monthly maintenance fees to eat away at your gains.

- Low or no minimum balance requirements for maximum flexibility.

- An easy-to-use mobile app for quick and seamless transfers.

Having three to six months of expenses tucked away in an HYSA provides a psychological safety net that is truly priceless. It prevents you from raiding your long-term investments or using high-interest credit cards when life throws an unexpected curveball. Think of it as your financial ‘peace of mind’ bucket that actually pays you to keep it full and ready. In today’s digital age, opening one takes less than ten minutes but pays dividends for many years to come. Don’t let your money sit idle in a standard account when it could be growing for you!

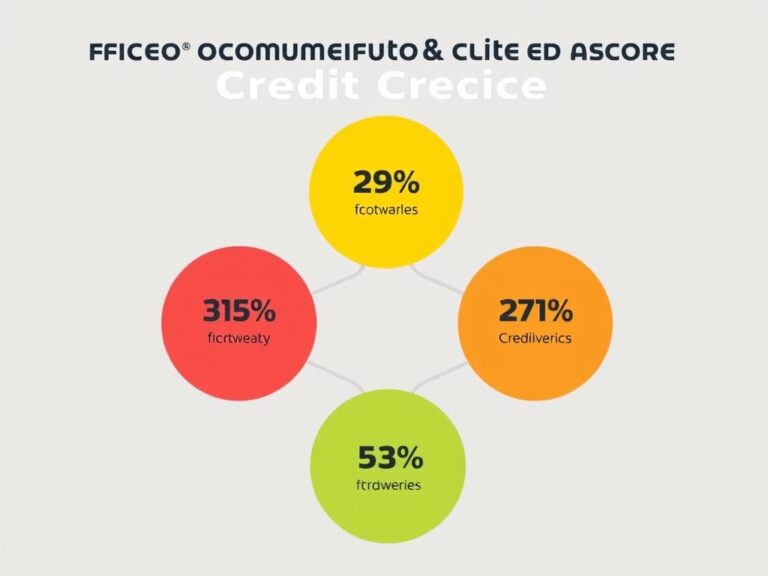

Now, let’s dive into a topic that many find intimidating but is actually quite logical once explained: Credit Scores. 💳 Your credit score is essentially your ‘financial GPA,’ and it dictates how much you will pay for major life milestones like buying a home. The most important factor in your score is your payment history, making up a whopping 35% of the total calculation. Another critical component is credit utilization, which is the ratio of your current credit card balances to your total available limits. Ideally, you want to keep this utilization under 30% to show lenders you can manage credit responsibly without being overextended. Here are a few expert tips to boost your score naturally:

- Set up autopay to ensure you never miss a single due date.

- Keep old accounts open to increase your total credit history length.

- Check your credit report annually for any errors or inaccuracies that might hurt you.

Having a high score can save you tens of thousands of dollars in interest over the life of a mortgage. It is not about being in debt; it is about demonstrating reliability and financial discipline to the financial world. A stellar credit profile opens doors to premium credit cards with travel rewards and lucrative cash-back perks. Treat your credit like a valuable asset, and it will serve you well for a lifetime of lower costs. If your score is low right now, don’t worry—consistent positive habits can turn it around faster than you might think.

Finally, we must address the ‘invisible tax’ that eats away at your purchasing power every single year: Inflation. 🎈 Inflation occurs when the general price of goods and services rises, meaning each dollar you own buys fewer items than it did yesterday. To stay ahead of inflation, you cannot simply save your way to true wealth; you must eventually invest in assets. While cash is great for liquidity and emergencies, holding too much of it for too long is a guaranteed recipe for losing value. Expert investors focus on things like diversified stocks, real estate, or inflation-protected securities to preserve and grow their wealth. The goal is to achieve an annual return that exceeds the current inflation rate, keeping your real net worth growing consistently. Think of it this way: if inflation is 3% and your bank account pays only 0.1%, you are effectively losing 2.9% of your wealth annually. Understanding this concept shifts your mindset from ‘saving’ to ‘building,’ which is a crucial transition for long-term financial success. Education is your best defense against economic shifts, so stay informed about market trends and interest rate changes. By diversifying your assets, you create a powerful hedge that protects you during volatile economic periods and recessions. Personal finance is a marathon, and managing inflation is how you ensure you finish the race strong and wealthy. You now have the tools and the knowledge to build a robust financial future for yourself starting today!