Budgeting, High-Yield Savings, Credit Score & Inflation: Personal Finance Tips

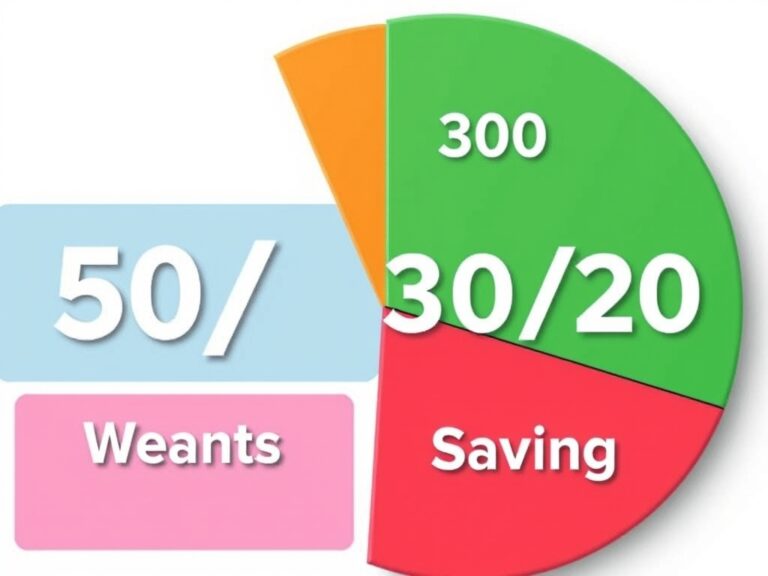

Mastering your budget is the cornerstone of all personal finance tips because it provides a clear vision of where your money actually goes. Instead of viewing a budget as a restrictive cage, try to see it as a tool that grants you permission to spend guilt-free on things you love. To get started, I highly recommend the 50/30/20 rule to simplify your monthly cash flow management. This rule suggests that you:

- Allocate 50% of your income to absolute essentials like rent, utilities, and groceries.

- Use 30% for wants, such as dining out, hobbies, and streaming services.

- Dedicate the remaining 20% strictly to savings, investments, and debt repayment.

Tracking your expenses manually or through an automated app can reveal surprising patterns in your spending habits. Many people find they are spending hundreds on phantom subscriptions they no longer even use. Once you identify these leaks, you can redirect that capital toward your long-term wealth goals. Remember that a budget is a living document that should evolve as your life changes and grows. It is not about being perfect from day one, but about becoming more intentional with every dollar. Consistency is the secret sauce that transforms a simple list of numbers into a powerful engine for financial freedom. By the end of the first month, you will likely feel a profound sense of control over your lifestyle. This control is the foundation upon which you will build the rest of your financial empire.

Once your budget is flowing smoothly, the next step is to make sure your cash is working just as hard as you do. Most traditional brick-and-mortar banks offer dismal interest rates that barely move the needle on your balance. This is where High-Yield Savings Accounts (HYSA) become your most valuable ally in the quest for financial growth. These accounts often provide interest rates that are significantly higher than the national average, allowing your money to grow passively through the power of compound interest. Compound interest is a mathematical miracle that helps your interest earn even more interest over time, effectively snowballing your wealth. For an emergency fund, an HYSA is the perfect home because it keeps your money liquid while still outperforming inflation. Always ensure the institution you choose is FDIC-insured so your hard-earned capital remains safe and secure. Setting up an automatic transfer from your checking account to your savings can help you build wealth without even thinking about it. Imagine waking up to find that your bank paid you just for keeping your money in the right place! It is one of the easiest ways to optimize your personal finance strategy with minimal effort. Don’t leave your money sitting idle in a basic checking account where it loses value every single day. Take fifteen minutes today to compare the top online banks and switch to a high-yield option. This simple change is a foundational block of expert-level money management that anyone can implement.

Your credit score is essentially your financial GPA, and it plays a massive role in your overall economic health and borrowing power. A stellar score can save you tens of thousands of dollars over the life of a mortgage or an auto loan by securing lower interest rates. To keep your score in the ‘excellent’ range, you must understand that payment history is the most critical factor, making up 35% of your total score. Even a single late payment can cause a significant dip that takes months or even years to fully recover from. Another vital metric is your credit utilization ratio, which measures how much of your available credit you actually use versus your limits. Financial experts generally recommend keeping this ratio below 30%, though staying under 10% is even better for your profile. Avoid the temptation to close your oldest credit card accounts, as the length of your credit history adds crucial stability to your score. Regularly monitoring your credit report allows you to catch errors or signs of identity theft before they cause lasting damage. Think of your credit as a long-term asset that requires consistent maintenance and responsible behavior. Using credit cards for daily purchases can be beneficial, provided you pay the full balance every month to avoid interest. This strategy allows you to earn rewards while building a robust credit profile simultaneously. If you are just starting, consider a secured credit card to begin building your reputation with lenders safely. Each small improvement you make today sets the stage for massive financial opportunities tomorrow.

We cannot discuss personal finance without addressing the elephant in the room: inflation. Inflation is the gradual increase in prices, which effectively reduces the purchasing power of your currency over time. If your income or your savings interest rates aren’t keeping pace with inflation, you are technically losing wealth every year. To protect yourself, you need to move beyond simple saving and start looking into strategic investing to preserve your future. Diversification is your primary defense mechanism against the volatile nature of economic cycles and price spikes. Stocks historically outperform inflation over long periods by growing alongside the economy. Property values and rents typically rise alongside inflation, providing a natural hedge in a balanced portfolio. Keep an eye on the Consumer Price Index (CPI) to understand how the cost of living is shifting in your area. High inflation periods require you to be more disciplined with your ‘wants’ in your 50/30/20 budget. It is also a great time to negotiate for a raise or look for side income to maintain your standard of living. Remember that inflation is a normal part of a growing economy, but it requires an active management strategy. Stay patient during market downturns, as panic selling is the quickest way to lock in permanent losses. By staying informed and adaptable, you can navigate even the most inflationary environments with total confidence.

Bringing all these elements together—budgeting, savings, credit, and inflation hedges—creates a holistic financial plan that can withstand any economic weather. Personal finance is rarely about a single ‘lucky break’ and usually about the cumulative effect of small, smart choices made daily. Start by auditing your current situation and setting specific, measurable goals for the next twelve months. Whether you want to wipe out debt, buy a home, or build a retirement nest egg, the principles of consistency remain the same. Use technology to your advantage by setting up alerts for bill payments and tracking your net worth regularly. Don’t be afraid to seek professional advice if your situation becomes complex or if you feel overwhelmed by the options. Education is an ongoing journey, so make it a habit to read financial news or listen to expert podcasts. The most important step you can take is the very first one, regardless of how small it might seem today. You have the tools and the knowledge now to take charge of your financial future and build lasting wealth. Financial peace of mind is one of the greatest gifts you can give to yourself and your family. Stay disciplined, stay focused on your ‘why,’ and watch as your financial dreams slowly become your reality. Thank you for taking this time to invest in your own growth and financial literacy today. Remember, the journey to wealth is a marathon, not a sprint, so celebrate every milestone along the way!